- Market Overview

- Futures

- Options

- Custom Charts

- Spread Charts

- Market Heat Maps

- Historical Data

- Stocks

- Real-Time Markets

- Site Register

- Mobile Website

- Trading Calendar

- Futures 101

- Commodity Symbols

- Real-Time Quotes

- CME Resource Center

- Farmer's Almanac

- USDA Reports

Should You Buy the Post-Earnings Pop in Kohl’s Stock?

Kohl’s (KSS) has recently captured the spotlight on Wall Street, with its stock catapulted by 24% following its second-quarter earnings release on Aug. 27, buoyed by better-than-expected earnings and a revised full-year forecast. This unexpected rally, fueled by cost discipline, margin improvements, rising proprietary-brand and Sephora sales, and even meme-stock momentum, has reignited investor interest.

However, Kohl’s still faces structural headwinds from ongoing same-store sales declines, lingering management turnover, and a fragile retail landscape. So, let’s analyze whether the surge reflects durable strength or a fleeting market reaction.

About Kohl’s Stock

Kohl’s is a prominent American department store chain headquartered in Menomonee Falls, Wisconsin. The company operates over 1,100 stores nationwide alongside a growing e-commerce platform and has a market cap of $1.8 billion. Its product offerings span several key segments: apparel; footwear; accessories and jewelry; beauty and personal care; and home goods, including furniture, décor, and household items.

Kohl’s share price stands at $15.20 as of Friday afternoon, following a remarkable 24% intraday surge on Aug. 27 after the retailer topped Wall Street’s fiscal second-quarter earnings expectations and revised its guidance. This powerful rally helped erase much of the weakness seen earlier in the year, and the stock now reflects an 8.16% year-to-date (YTD) return, signaling a sharp turnaround from its prior stumbles.

Despite this recovery, Kohl’s remains well below its 52-week peak of $21.39 reached on July 22, following a 37.6% single-day surge amid meme-stock–style activity and heavy short interest. The stock is down by 22% over the past year.

While the stock is trading at a premium compared to industry peers at 37.70 times forward earnings, it is trading below the sector median in terms of price/sales (P/S) ratio at 0.09.

Kohl’s Q2 Results Surpassed Projections

Kohl’s released its second-quarter fiscal 2025 earnings on Aug. 27, covering the period that ended on Aug. 2. Despite a challenging environment, the company delivered adjusted earnings per share (EPS) of $0.56, significantly above analysts’ expectations but below the prior-year quarter value of $0.59.

On the top line, net sales declined by 5.1% year-over-year (YoY) to $3.3 billion, while comparable-store sales dropped 4.2%. However, gross margin improved by 28 basis points, reaching 39.9%, and SG&A expenses fell 4.1%, illustrating effective cost management.

Key strategic drivers during the quarter included sales growth from proprietary brands, the Sephora at Kohl’s rollout, and improvements from impulse purchase areas, which helped offset some top-line weakness. Additionally, inventory was reduced by 5%, further supporting its performance.

Looking ahead, Kohl’s upgraded its full-year guidance for 2025. The company now anticipates a net sales decline of 5% to 6%, with comparable sales down 4% to 5%, and expects adjusted EPS in the range of $0.50 to $0.80, up from its prior EPS outlook of $0.10 to $0.60.

Analysts remain bearish as they predict EPS to be around $0.58 for the current fiscal year, down 61.3% YoY, before declining by another 41.4% annually to $0.34 in the next fiscal year.

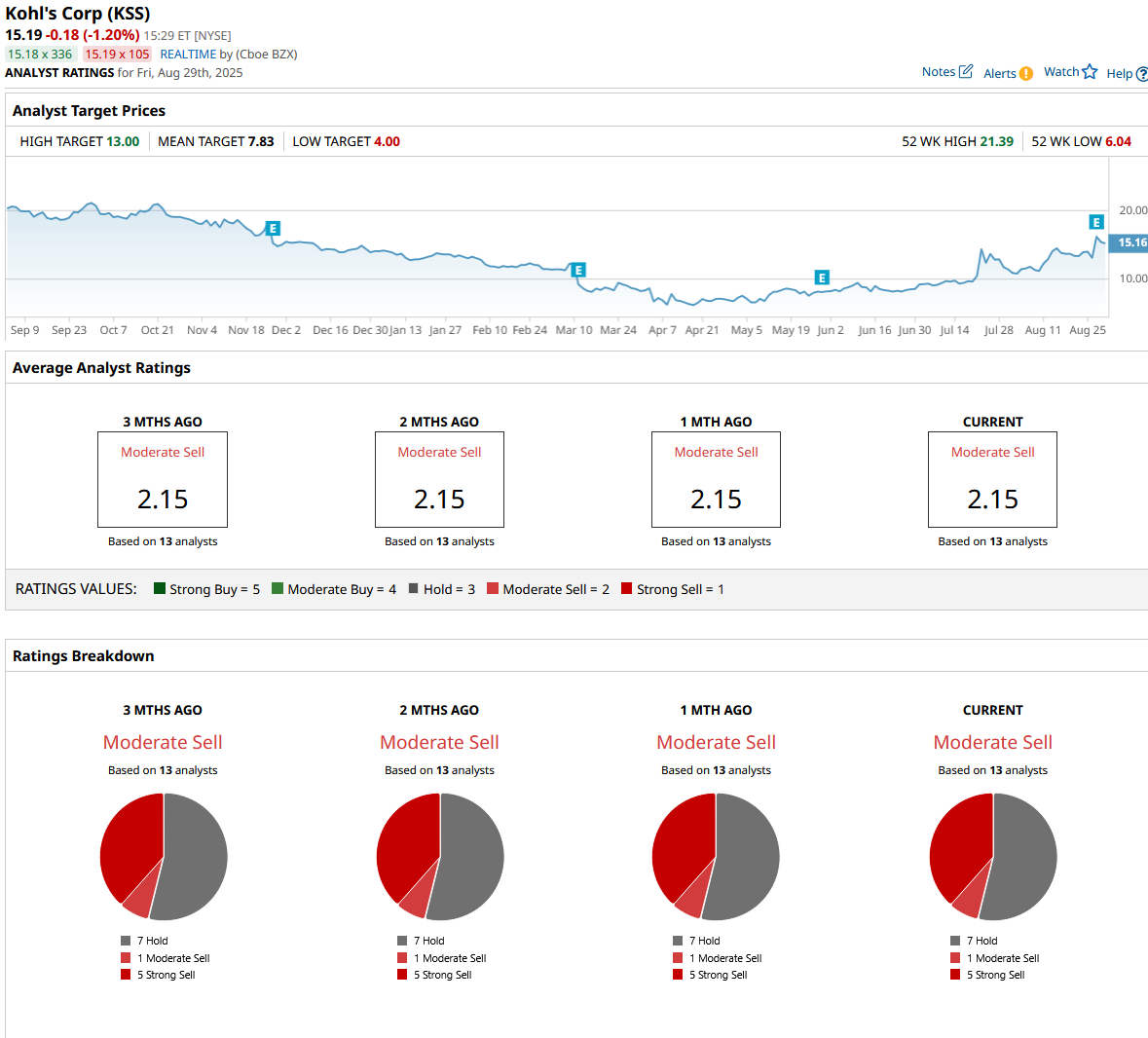

What Do Analysts Expect for KSS Stock?

Analyst sentiment toward Kohl’s has turned notably cautious in recent months, despite some raising the price targets for the stock.

Recently, BofA Securities raised its price target on Kohl’s to $8.4 from $7 but maintained an “Underperform” rating, despite the stock’s strong momentum. BofA cautioned that credit upside will turn into a headwind in the second half, pressuring earnings, and kept a cautious outlook given weak comparable sales and macro challenges.

Also, earlier this month, UBS reaffirmed its “Sell” rating on Kohl’s, with a $4 price target, signaling continued concern over the retailer’s competitive pressures and related headwinds.

Wall Street is majorly bearish on KSS. Overall, KSS has a consensus “Moderate Sell” rating. Of the 13 analysts covering the stock, seven advise a “Hold,” one suggests a “Moderate Sell,” and the remaining five analysts recommend a “Strong Sell” rating.

The average analyst price target for KSS is $7.83, indicating a potential downside of 48%. The Street-high target price of $10 also suggests that the stock can plunge as much as 34%.

On the date of publication, Subhasree Kar did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.